BBS 3rd Year Tax Notes PDF 2082 | Complete Income Tax & VAT Notes for TU

This includes:

- BBS 3rd Year

- Tax Notes

- 2082

- TU

BBS 3rd Year Taxation Notes 2082 are specially prepared for students of Tribhuvan University (TU) according to the latest syllabus. These notes cover complete Income Tax and Value Added Tax (VAT) concepts with practical examples and exam-oriented solutions.

Our BBS 3rd Year Tax Notes PDF includes detailed explanation of income classification, tax computation, depreciation, deductions, capital gain tax, investment income, assessment procedure, tax administration, and VAT system in Nepal.

These notes are highly useful for:

- TU final exam preparation

- Back and improvement students

- Chapter-wise revision

- Conceptual understanding of Nepal tax system

Download BBS 3rd Year Taxation Notes PDF 2082 and prepare effectively for your board examination.

The course contains BBS 3rd year Taxation in Nepal

BBS 3rd Year Tax Syllabus Tax Notes PDF

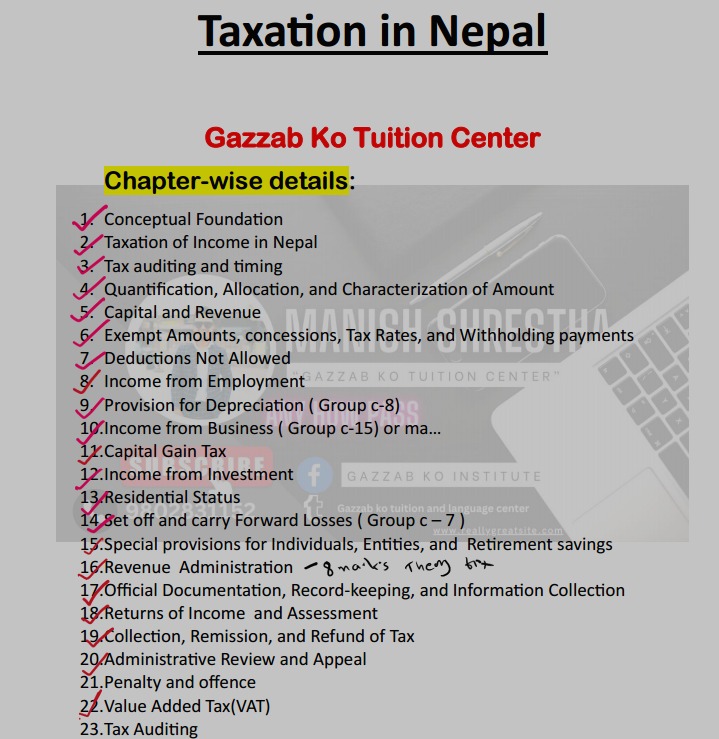

Chapter-wise Details – BBS 3rd Year Taxation

- Conceptual Foundation

- Taxation of Income in Nepal

- Tax Auditing and Timing

- Quantification, Allocation, and Characterization of Amount

- Capital and Revenue

- Exempt Amounts, Concessions, Tax Rates, and Withholding Payments

- Deductions Not Allowed

- Income from Employment

- Provision for Depreciation (Group C-8)

- Income from Business (Group C-15)

- Capital Gain Tax

- Income from Investment

- Residential Status

- Set Off and Carry Forward Losses (Group C-7)

- Special Provisions for Individuals, Entities, and Retirement Savings

- Revenue Administration

- Official Documentation, Record Keeping, and Information Collection

- Returns of Income and Assessment

- Collection, Remission, and Refund of Tax

- Administrative Review and Appeal

- Penalty and Offence

- Value Added Tax (VAT)

- Tax Auditing

BBS 3rd Year Taxation Notes 2082 PDF | TU Updated

BBS 3rd Year Taxation in Nepal Notes

Income from employment BBS 3rd Year Tax

Download Income from Employment Format

BBS 3rd Year Taxation in Nepal: All chapters Youtube Video link

Provision for depreciation BBS 3rd Year

Provision for depreciation Numerical notes

Withholding Income Tax Payment

Taxation of Income

Withholding Payment [Advance TDS and Final TDS)

Advance vaya= hisab garda goross up garera rakhne

Final Vaya = Hisab garda xodidine

Rate of withholding payments

| Withholding payments | TDS Rate | Advance/Final |

| Natural resource payments, royalties, commission, service fee, bonus etc income received | 15% | Advance |

| Dividend paid by resident company, Bank | 5% | Final |

| Dividend paid by foreign company | As per tax credit rule | Advance |

| Interest received by individual from resident bank, company not related to business | 6% | Final |

| Interest received by Life insurance company from resident bank | 5% | Advance |

| Interest received by non-life insurance company, cooperatives etc. | 15% | Advance |

| Interest received by Microfinance company from Bank | 0% | No TDS |

| Interest received by individual from private party, unauthorized party in general | 15% | Advance |

| Rent received by individual(net) after TDS, let out | 10% | Final |

| Rent received from staff quarter, House sub let –out | 10% | Advance |

| Meeting allowance | 15% | Final |

| TADA, Saving from TADA | 0% | Not Taxable |

| Part time teaching, casual basis work, payment for question making , checking paper, examiner fee, setting paper | 15% | Final |

| Retirement payment from approved retirement fund. | 5% | Final |

| Gain from mutual fund, mature Investment insurance | 5% | Final |

| Retirement payment from unapproved retirement fund. | 5% | Final |

| Payment commission by resident company to non-resident | 5% | Final |

| Payment tuition fee by resident person to foreign university. | 3% | Final |

| Payment of service fee, Contract payment | 1.5% | Advance |

| Lease payment | 10% | Advance |

| Casual gain/windfall gain | 25% | Final |

| Gain from commodity market | 10% | Advance |

| Gain from sales of listed share less than 365 days-Individual | 7.5% | Advance |

| Gain from sales of share more than 365 days- individual | 5% | Advance |

| Gain on sale of share(securities) listed- Entity | 10% | Advance |

| Gain sale of listed or non-listed share- Non-resident or other | 25% | Advance |

| Gain on sale of non-listed share- Individual | 10% | Advance |

| Gain on sale of non-listed share -Entity | 15% | Advance |

| Gain of sale of Land and Building ownership less than 5 year | 7.5% | Advance |

| Gain of sale of Land and Building ownership more than 5 year | 5% | Advance |

| Gain of sale of non-business chargeable Assets( Machine, Furniture) | 10% | Advance |

Tax Unit 2 Theory

Chapter 2: Tax Accounting

Tax Accounting is the recording of financial transaction for tax purpose. Tax accounting are prepared on the basis of tax law and quite difference than account statement of financial accounting. Tax accounting applied for individuals, entity, company, cooperation’s and other business firm. Tax accounting follows Generally accepted accounting principle(GAAP).

The Tax accounting is recognized on the basis of cash as well as accrual basis of income and expenses.

Basis of Accounting

| Person/Company | Income Head | Accounting Basis |

| Individual person | Employment | Cash Basis |

| Individual Person | Investment | Cash or Accural Basis |

| Partnership company | Business/Investment | Cash/Accural Basis |

| Company | Business | Accural Basis |

| Sole Traders | Business | Accural or cash |

| Banking and financial institution | Investment | Accural Basis Interest income: accrual Interest expenses: Cash |

Partnership business more than 20 partner –Accural Basis

Less than 20 Partners — cash/Accural Basis

Cash Basis: calculation of income and expense is kept while cash is received or paid.

Accural Basis: Calculation of income and expense is kept at the time of expenses and income incurred for particular month /year.

Unit 13 Residential Status Question Solution with format

Income from business format BBS 3rd year Taxation in Nepal

Income from business format part ii

Income from Business 2081 model question solved

Income from Business 2080 Model question solved

Income from Business 2079 Model question solved

Income from Business solve 2081,2080,2079,2076,2066 and from books

H1: BBS 3rd Year Taxation Notes 2082 PDF Download

H2: Chapter-wise Details – BBS 3rd Year Taxation

H2: Income Tax Notes for BBS 3rd Year

H2: VAT Notes for BBS 3rd Year

H2: Numerical and Theory Solutions

H2: Frequently Asked Questions

Add FAQ Section (Very Powerful for Ranking)

Add this at bottom:

Q1. Where can I download BBS 3rd Year Taxation Notes 2082 PDF?

Q2. Are these notes updated according to TU syllabus?

Q3. Does it include numerical and theory questions?

Q4. Is VAT included in BBS 3rd Year Tax Notes?

Google shows FAQ in search results → more clicks

Internal Linking Strategy

On this page, link to:

- BBS 3rd Year Finance Notes

- BBS 3rd Year Business Law Notes

- BBS 3rd Year Marketing Notes

- BBS 3rd Year Strategy Notes

BBS 3rd Year Tax Notes PDF

TU BBS Taxation Notes 2082

Income Tax Notes BBS 3rd Year

VAT Notes BBS 3rd Year

BBS 3rd Year Tax Numerical PDF

Website / Information Hub: https://gazzabkosir.xyz/ — This is the main site where you can find class details, notes, schedules, PDFs, exam tips, and more related to Gazzab Ko Tuition Center.

📱 YouTube & Learning Videos: Gazzab Ko Tuition Center also has a YouTube channel with free educational videos and tutorials — you can search “Gazzabko Tuition Center” on YouTube to find it.

Contact Phone: +977 9802831152 / +977 9841414845 (from info shared on their website).

Location: Suryabinayak Chowk, Bhaktapur, Nepal (near Thimi area).

If you want direct links to specific content (like PDFs, class recordings, or WhatsApp groups), tell me what you’re looking for — I can fetch those for you as well!